Average Costing

Introduction

What Is Average Costing?

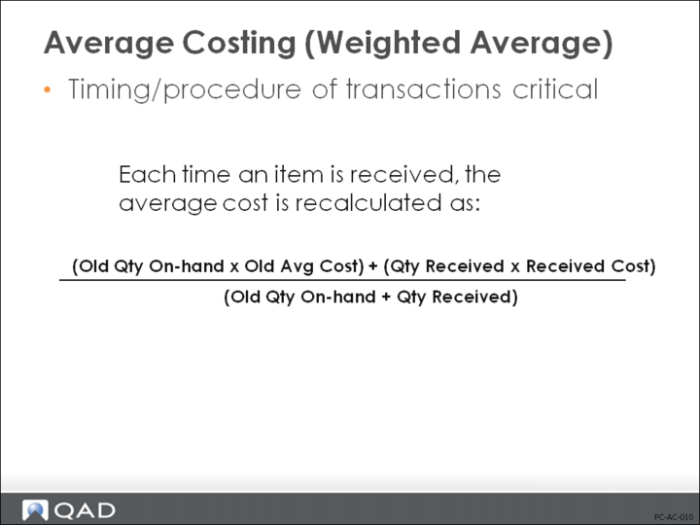

Average costing simply keeps a running average of what an item is costing. This is much different than standard costing, which predicts what an item should cost. With the average cost method, the average cost of the goods available for sale is not predefined by you; rather it is computed and the units in both cost of goods sold and ending inventory are costed at this average cost. It is a weighted average: Each unit cost is weighted by the number of units with that cost (see figure above). In QAD Enterprise Applications, a new average unit cost is calculated after each receipt and optionally by AP supplier invoices.

How to Set Up Average Costing

Use QAD Enterprise Applications Cost Management to set the GL cost set to have a costing method of Average Cost. To create a cost set type GL with its method set to Average, it is necessary to create a new cost set by using Cost Set Maintenance (30.1) because you cannot modify the default GL Standard cost set. You can only set the cost set type when adding a new cost set. When you have created the new cost set of the type GL with the method Average, you can populate it with data, if you choose, by copying another cost set using Cost Set Copy to Cost Set (30.3). This new GL Average cost set can now be assigned to the appropriate sites by using Cost Set to Site Assignment (30.9).

Average Cost Considerations

In order to successfully use average costing, you need to maintain perpetual inventory balances, both in terms of quantity and for accounting purposes. The system assumes that the following is true.

• You must maintain physical inventory on a perpetual basis. When items are issued from inventory, the on-hand quantity is immediately decreased. When items are received on purchase orders or manufacturing orders, the on-hand quantity is immediately increased.

The timing of transaction entry is absolutely vital. Because averaging is done based on quantity on-hand, these quantities must be accurate. Also, if you are using Cost by Operation Report, all components should be issued for the entire work order quantity prior to moving work to the next operation; otherwise costs will be misstated on this report.

• You must maintain accounting inventory on a perpetual basis. When items are issued from inventory, the Inventory account is immediately credited and the WIP or COGS accounts are debited. When items are received on purchase orders or manufacturing orders, the Inventory account is immediately debited and the WIP or PO Receipts account is immediately credited.

• You must not allow negative inventory balances. Use Inventory Status Codes to prevent overissuing. As you can see from the calculation a negative balance times the old average cost will yield a negative cost which when averaged with the new items at their cost will result in an answer that does not make sense. To prevent this in the case of a negative on-hand the system uses the current receipt cost.

Once again, timing is important. If GL transactions are not generated immediately, they will not pick up the correct cost because cost changes each time a receipt is processed.

The accounting balance for inventory should at all times be equal to the quantity in inventory multiplied by today’s average cost for the item. This ensures that the Inventory subsidiary ledger always balances to the general ledger.

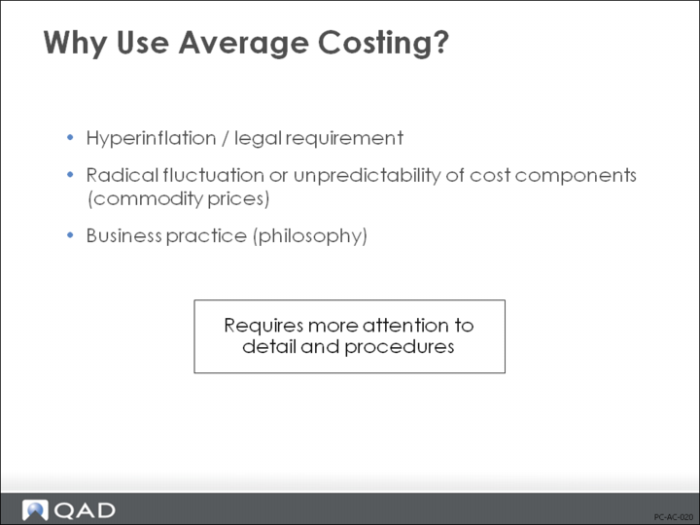

Why Use Average Costing?

Average costing is primarily used in two situations:

• Hyperinflationary economies (where it might be a legal requirement)

• Commodity-based manufacturing environments

In both of these situations, it is almost impossible to predict what item costs should be (standard cost). In a hyperinflationary economy, prices rise explosively with inflation. In a commodity-based environment, commodity prices can fluctuate wildly. This is the case for many process manufacturers.

Example: A food processing company whose major ingredient is sugar can choose not to use standard costing because sugar prices normally cannot be predicted very accurately from one day to the next. Yet the company still needs to track sugar’s actual price to accurately cost products and determine revenues.

In these types of environments, average costs are used. They track the movement of costs, on average, and provide a more realistic view of what inventory values and cost of sales actually are.

Note: Be aware that, as with any actual costing technique, average costing requires much more reporting detail than standard costing and requires much stricter procedural controls.

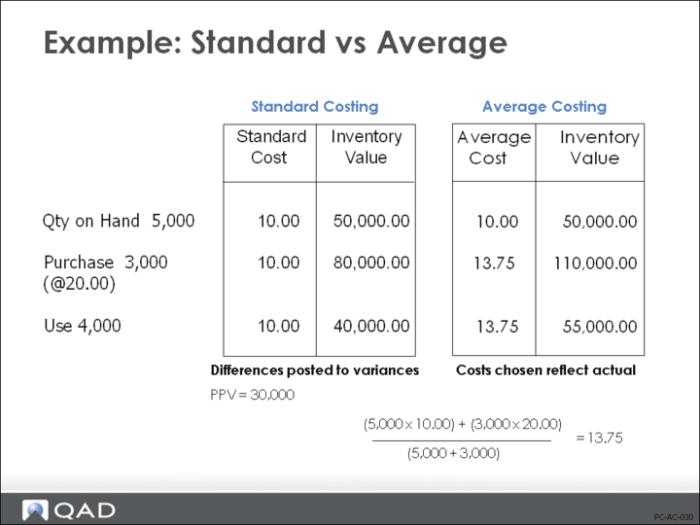

Example: A company has an initial inventory of 5,000 items that cost 10.00 each for an on-hand value of 50,000.00. This is a commodity item whose purchase price varies widely. The company wants to compare the difference affects of standard versus average costing. The beginning balance of 50,000.00 is the same for either method.

If the company uses standard costing, with the standard set at 10.00 and purchases an addition 3,000 units at a cost of 20.00 each the value of inventory is 80,000.00, that is 8,000 units at the standard cost of 10.00. There is a purchase price variance of 30,000.00.

The cost of manufacturing would be understated (and revenue would be overstated).

Under an average cost system, the cost is re-averaged at the time of receipt.

[(5,000 * 10.00) + (3,000 * 20.00] / (5,000 + 3,000) = 13.75

The new value in inventory would be (13.75 ∗ 8,000) or 110,000.00; a more accurate reflection of its cost.

Issues from inventory do not change the average value of the items just the total value on-hand.

Standard costs can be used in an inflationary or commodity-based environment, but it is necessary to change standards very frequently (perhaps weekly or monthly).