Realized Gain and Loss

For payments in base or transaction currencies, the system calculates the realized gain or loss in base currency and in statutory currency, and posts the difference to the relevant gain or loss system accounts. The gain or loss is the difference between the base currency (or statutory currency) value of the invoice at the time it was created and the base currency (or statutory currency) value of the invoice at the time of payment. For partial payments, this difference is prorated according to the amount paid.

When a domain uses a statutory currency, the system calculates the gain or loss twice, once for the base currency and a second time using the statutory currency, each using the most recent statutory exchange rate.

The original exchange rates for both the base currency and statutory currencies are stored in the original transaction invoice record, and compared with the relevant exchange rate at the time of payment. The difference is then posted as a gain or loss.

The differences in the base currency calculations and statutory currency calculations for the same transactions can have a different sign. For example, the same transaction can cause a gain in base currency and a loss in statutory currency. In this case, two posting lines are created: one for the gain amount and one for the loss amount.

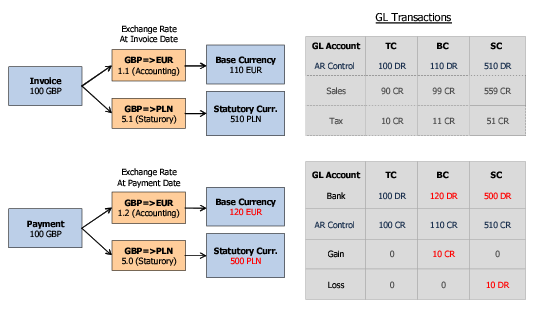

Example:

A domain has a base currency of Euros and a statutory currency of Polish Zloty (PLMN). The company sells 10 items to a British customer at a unit cost of 10 GBP each.

When the invoice is posted, the system posts a debit of 100 GBP to the AR control account and uses the accounting exchange rate of 1.1 to convert this amount to Euros for the base currency (110 Euros). It then uses the statutory exchange rate of 5.1 to convert from GBP to PLN (510 PLN). The sales account is credited with 90 GBP (equivalent to 99 Euros and 559 PLN) and the tax account is credited with 10 GBP (equivalent to 11 Euros and 51 PLN).

When the customer pays the invoice, the exchange rates have changed. The accounting rate from GBP to Euros is now 1.2 and the statutory rate from GBP to PLN is now 5.0. When the payment is lodged in the bank account, 100 GBP is equivalent to 120 Euros and 500 PLN. However, the payment postings to the AR control account use the exchange rates valid at the invoice date (accounting rate 1.1 and statutory rate 5.1). Therefore, the AR control account is credited for 100 GBP, which is equivalent to 110 Euros and 510 Zloty.

The system posts a realized gain of 10 Euros to the Realized Gains account and a loss of 10 Zloty to the Realized Loss account.

Realized Gains and Loss in Statutory and Base Currencies