Consolidation

Objectives

Overview

This section reviews the highlights of the consolidation functionality in QAD Enterprise Applications, including its benefits and current scope.

We will then study the consolidation process—from setup to processing—in more detail.

Finally, you will practice your newly-acquired knowledge with a hands-on exercise.

Consolidation Benefits

Consolidation is usually a monthly review process, giving an immediate financial summary of a multi-entity organization.

You can perform a number of consolidations within the organization to account for subsidiaries that have been taken over by the parent organization.

In order to consolidate, you must identify the entities with accounts you want to consolidate, and set up a consolidation entity in which to store the consolidation data. All accounts in the source entities are mapped to corresponding consolidation accounts in the consolidation entity.

The consolidation functionality responds to a legal and accounting requirement.

Current Scope

The consolidation functionality requires that the entities to consolidate be in the same database, but they can belong to different domains.

You can, optionally, include the full GL analytic detail in a consolidation, for example, sub-account, cost center, project, and SAF structures, or only part of it.

The entities involved in consolidation do not need to have the same base currency.

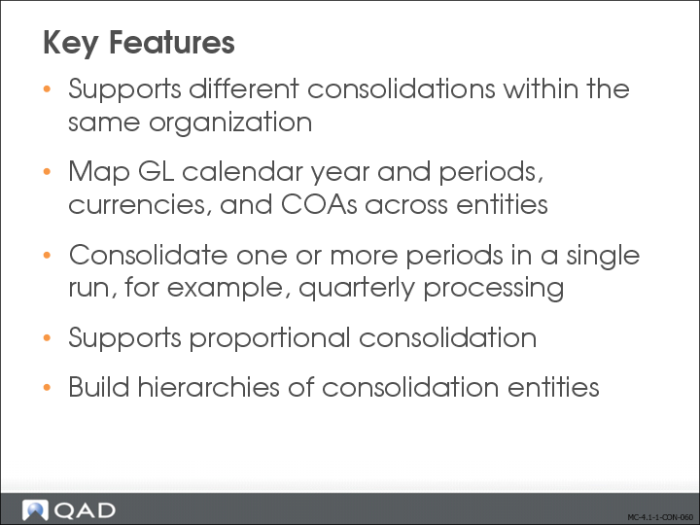

Key Features

The consolidation functionality in QAD Enterprise Applications lets you perform multiple consolidations within one system, and is, therefore, of great benefit to large organizations,

Again, you can include all GL analytical elements in a consolidation.

Proportional consolidation is an option, and we will review this later in more detail.

The entities involved in a consolidation do not need to have to have the same GL calendar. Additionally, a consolidation can be run for one or several periods at a time.

In a consolidation entity, the same reporting capabilities exist as for non-consolidation entities.

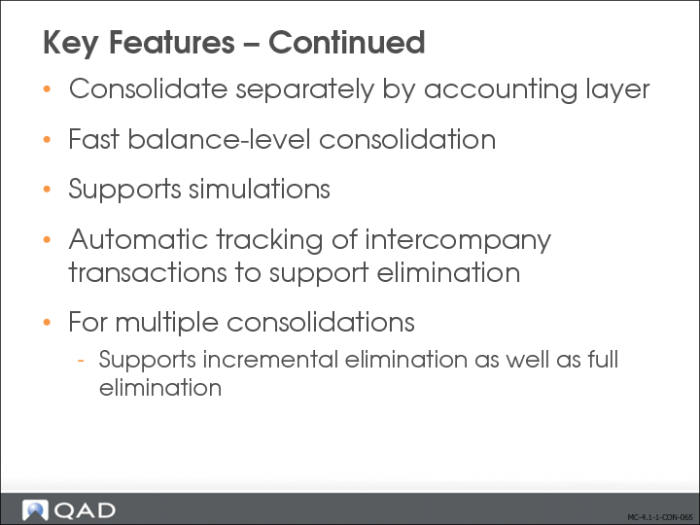

Key Features — Continued