Standard Costing: Example

A standard cost for a product consists of a price standard (price for material; rate for labor and manufacturing burden) and a quantity standard (quantity for material; time for labor; quantity or volume for manufacturing burden). The combination of price and quantity yields what is planned or expected for a specific interval of time and set of conditions. Cost for Overhead and Subcontract costs are set up and included in the Inventory value.

• Setting standards for price and quantity involves management judgements, industrial engineering studies, work measurement studies, vendor analyses, as well as a number of other techniques

Once set, the standard cost of an item is used as the basis for all accounting entries for inventory related transactions (see figure above). Standard costs cover a specific period, usually a year. They can evaluated and changed at any time.

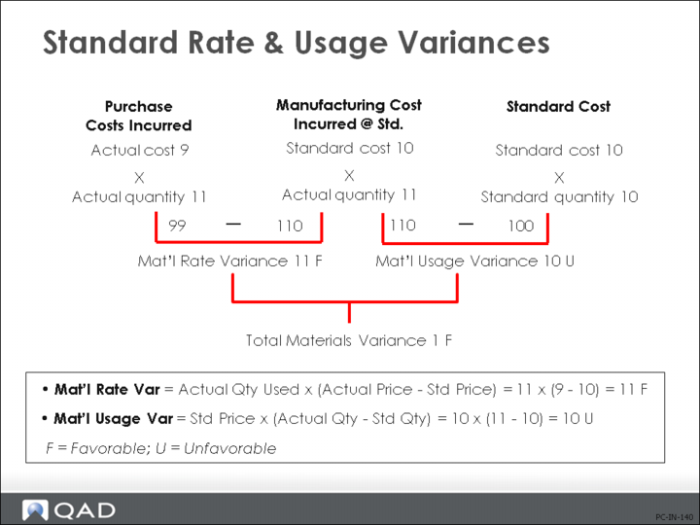

Standard Cost: Variances

Because the standard is only a target or estimate of what an item will cost, the costs incurred rarely match the standard exactly. In order to account for the difference between standard costs and actual costs, variances are calculated and recorded.

• Variances are calculated as the difference between Standard and Actual costs and are defined as Total Variance. Total Variance can be subdivided into Price and Efficiency components called Rate and Usage in QAD Enterprise Applications (see figure above).

• Price or rate variance occurs when the actual purchase cost of a resource differs from the standard rate and is calculated based on the actual quantity purchased.

• Usage or efficiency variance occurs when the actual quantity transacted is different than the standard quantity that was defined and calculated using the standard cost. For example, if quantities of components issued are different than those defined and calculated using the standard BOM, or additional non-standard components are issued.

Note: An adverse variance is not necessarily an indication of underachievement. For example, a corporation can make allowances in its operating budget for unfavorable variances if standard costs cover a long period of time. Conversely, a purchasing department can be sent a budgeted favorable price variance to achieve when operating in a “cost down” environment with its customers and suppliers.

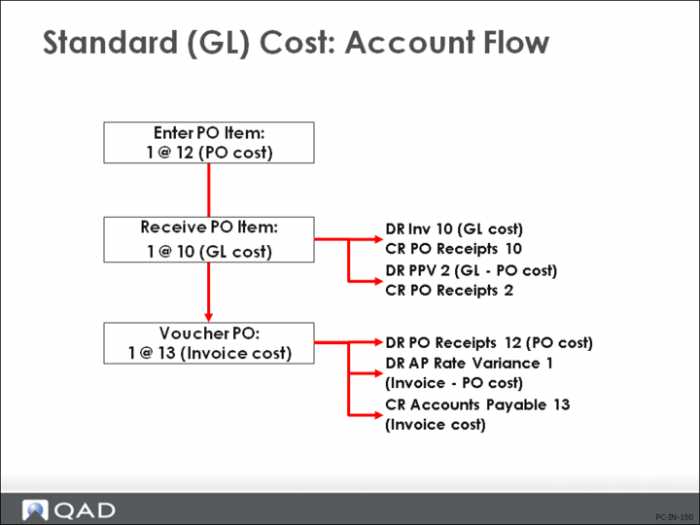

Standard (GL) Cost: Account Flow

Example: The example in the figure above shows how the general ledger uses variances to balance standard and actual costs. An item has a GL cost of 10. A purchase order is issued to purchase one for 12; its PO cost. When the invoice arrives, the supplier has charged 13.

• PO Receipt

When the item arrives, the Inventory account is debited for the 10 GL cost and the PO Receipts account is credited 10. The Purchase Price Variance account is debited 2 (the difference between the item’s PO cost and its GL cost) and the PO Receipts account is credited 2.

• Supplier Invoice Maintenance

An invoice is received and the supplier has charged 13 (1 over the PO cost) for the item. If it is decided to accept this increase and continue vouchering, the PO Receipts account is debited 12 (PO cost). The Accounts Payable account is credited 13 (invoice cost) and the Accounts Payable Rate Variance account is debited 1 (the difference between the PO cost and invoice cost).

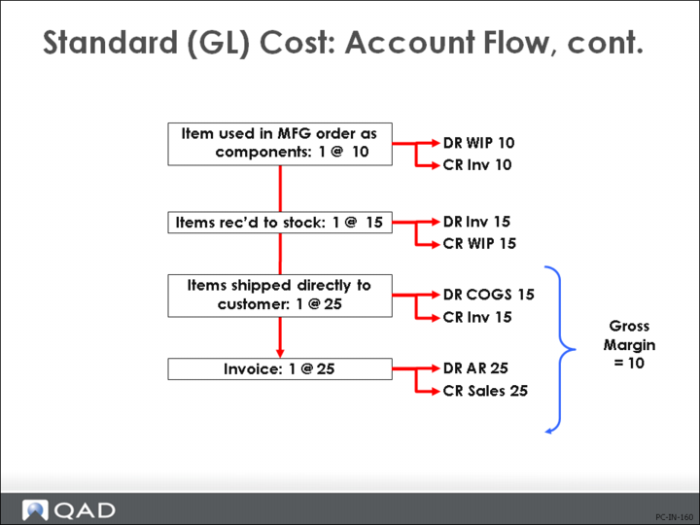

When items are taken from inventory and issued to manufacturing or shipped to a customer, the value of inventory is decreased at GL cost. Let’s see what happens when the purchased pens are issued.

• Manufacturing

The item is issued to the work order. Inventory is credited 10 (issued to the work order). Work in Process (WIP) is debited 10. The cost of the process of 5 is added to component cost so that the end item cost is 15. WIP is debited and a recovery account (Labor/Burden/Overhead Absorption) is credited with 5. Inventory is debited and WIP is credited 15 at Work Order receipt time.

• Sales shipment

Items shipped from stock decrease (credit) the inventory value by 15. Cost of goods is debited 15. The actual selling price of 25 is not recorded until the invoice is created. The difference of 10 is the gross margin.

• Invoice

When you print and then post the invoice, you debit Accounts Receivable 25 and credit Sales 25