Reviewing Traditional Self-Billing

In the automotive industry, suppliers often do not send invoices to their customers. Instead, the customer remits a self-bill. This document details shipments received and amount due to the supplier for these shipments. The amount also reflects any deductions for defective or damaged parts, and any other pertinent credits due. This document is called a self-bill because the customer decides the payable amount instead of relying on an invoice from the supplier.

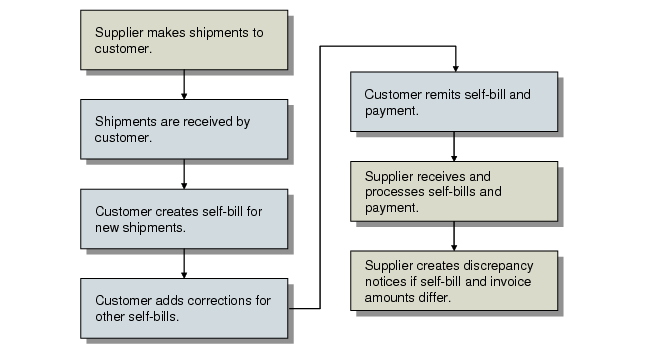

Traditional Self-Bill Work Flow shows the traditional self-bill work flow.

Traditional Self-Bill Work Flow

The self-bill is remitted to the supplier, who then processes it and compares it with open invoices. When the self-bill information is entered into the system, it is matched to invoices for that customer.

If the supplier notes any discrepancy between the self-bill and their records, the customer must be notified within a predefined period for corrections to be made. In some situations, a self-bill is remitted and only later is the payment made. In other situations, payment may accompany the self-bill.

The payment remitted reflects the self-bill and any agreed-upon corrections from previous self-bills. Each supplier-customer relationship usually sets up specific rules for reconciling discrepancies. Sometimes these must be written off as losses by either the supplier or the customer.