QAD 2017 Enterprise Edition

>

User Guides

>

Fixed Assets

>

Setting Up Fixed Assets

>

Depreciation Methods and Conventions

Depreciation Methods and Conventions

Using Depreciation Methods

Depreciation is the process of allocating the cost of an asset over its service life. There are several methods of calculating depreciation. Depreciation can be calculated one way for tax purposes and another for financial purposes.

Straight Line

Straight‑line depreciation allocates the asset cost evenly over its service life. The formula for straight‑line depreciation is:

Depreciation Charge = Depreciable Basis / Service Life

Depreciable Basis = Cost – Salvage Value

Example: A company purchases a $20,000 car that has a $2,000 salvage value and a five-year service life.

Straight‑Line Depreciation Schedule illustrates the straight‑line depreciation schedule.

Straight‑Line Depreciation Schedule

|

Year

|

Calculation

|

Depreciation Expense

|

|

1

|

$18,000 / 5

|

$3,600

|

|

2

|

$18,000 / 5

|

$3,600

|

|

3

|

$18,000 / 5

|

$3,600

|

|

4

|

$18,000 / 5

|

$3,600

|

|

5

|

$18,000 / 5

|

$3,600

|

Declining Balance

Declining balance is an accelerated method that provides higher depreciation charges in the earlier years of the asset life and lower depreciation charges in the later years.

The annual depreciation is calculated by using a constant depreciation percentage rate and multiplying it by the remaining net book value each year of the asset service life.

The formulas for declining‑balance depreciation are:

Depreciation Rate = Percentage Multiplier / Service LIfe

Depreciation Charge = Depreciation Rate * Net Book Value

Each year the net book value is calculated with the following formula:

Net Book Value = Net Book Value – Depreciation Expense

Example: A company purchases a $20,000 car that has a five-year service life. The company uses a percentage multiplier of 150% to calculate the depreciation for the automobile. The annual depreciation rate is calculated by annualizing the percentage multiplier over the automobile’s service life:

150% / 5 years = 30%

Declining‑Balance Depreciation Schedule illustrates the declining‑balance depreciation schedule.

Declining‑Balance Depreciation Schedule

|

Year

|

Net Book Value

|

Depreciation Rate

|

Calculation

|

Depreciation Expense

|

|

1

|

$20,000

|

30%

|

$20,000 * 30%

|

$6,000

|

|

2

|

$14,000

|

30%

|

$14,000 * 30%

|

$4,200

|

|

3

|

$9,800

|

30%

|

$9,800 * 30%

|

$2,940

|

|

4

|

$6,860

|

30%

|

$6,860 * 30%

|

$2,058

|

|

5

|

$4,802

|

30%

|

$4,802 * 30%

|

$1,441

|

With the declining‑balance method, $3,361 ($4,802 ‑ $1,441) of the asset cost is not depreciated. This amount is used to calculate a gain or loss at the time of retirement.

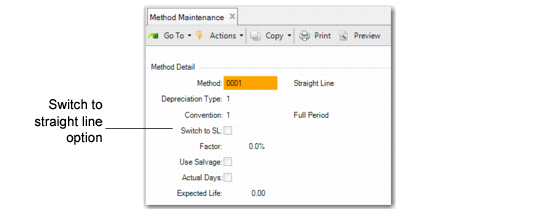

Declining Balance Switch to Straight Line

The standard declining‑balance method does not depreciate the asset to zero. You can choose to switch the declining‑balance method to the straight‑line method when the depreciation calculated by the straight‑line method is greater than the depreciation calculated by the declining‑balance method. This method fully depreciates the asset.

When you specify the switch to straight‑line method, the system uses a different calculation than for the standard straight-line method.

Depreciation Charge = (Depreciable Basis – Accumulated Depreciation) / Remaining Service Life

The system performs this calculation every year to compare the results against the declining balance. When the straight-line method yields higher annual depreciation, the calculation is switched.

Switch to Straight Line Option in Method Maintenance

Example: A company purchases a $20,000 car that has a $2,000 salvage value and a five-year service life. The company uses a percentage multiplier of 150% to calculate the depreciation for the automobile. The annual depreciation rate is calculated by annualizing the percentage multiplier over the automobile’s service life:

150% / 5 years = 30%

Declining‑Balance Switch to Straight‑Line Depreciation Schedule illustrates the depreciation charges for declining‑balance and straight‑line methods.

Declining‑Balance Switch to Straight‑Line Depreciation Schedule

Year | Declining-Balance Depreciation | Straight‑Line Depreciation | Declining-Balance Switch to Straight‑Line Depreciation | Accumulated Depreciation |

1 | $5,400 | $3,600 | $5,400 | $5,400 |

2 | $3,780 | $3,150 | $3,780 | $9,180 |

3 | $2,646 | $2,940 | $2,940 | $12,120 |

4 | N/A | $2,940 | $2,940 | $15,060 |

5 | N/A | $2,940 | $2,940 | $18,000 |

In year 3, the declining‑balance depreciation charge is less than the straight‑line depreciation charge. Therefore, the straight-line method will be used for the remaining years.

Sum of the Years’ Digits

Sum of the years’ digits is an accelerated method that provides a decreasing fraction to the asset depreciable basis.

The annual depreciation is calculated by applying a fraction to the asset depreciable basis. Each fraction uses the sum of the years’ digits as the denominator and the remaining years in the asset service life as the numerator. The numerator decreases each year while the denominator remains constant.

The formula for sum‑of‑the‑years’‑digits depreciation is:

Depreciation Charge = Depreciable Basis * (Number of Years Remaining / Sum‑of‑the‑Years’‑Digits)

Depreciable Basis = Cost – Salvage Value

Sum‑of‑the‑Years’‑Digits = 1 + 2 + n . . .

Example: A company purchases a $20,000 car that has a $2,000 salvage value and a five-year service life.

Depreciable Basis = $20,000 – $2,000 = $18,000

Sum of the Years’ Digits = 1 + 2 + 3 + 4 + 5 = 15

Sum‑of‑the‑Years’‑Digits Depreciation Schedule illustrates the sum‑of‑the‑years’‑digits depreciation schedule.

Sum‑of‑the‑Years’‑Digits Depreciation Schedule

Year | Remaining Life | Depreciation Fraction | Calculation | Depreciation Expense |

1 | 5 | 5 / 15 | $18,000 * (5 / 15) | $6,000 |

2 | 4 | 4 / 15 | $18,000 * (4 / 15) | $4,800 |

3 | 3 | 3 / 15 | $18,000 * (3 / 15) | $3,600 |

4 | 2 | 2 / 15 | $18,000 * (2 / 15) | $2,400 |

5 | 1 | 1 / 15 | $18,000 * (1 / 15) | $1,200 |

Flat Rate

Flat rate calculates depreciation by using a constant percentage and multiplying it by the depreciable basis over the asset service life until the sum of the depreciation is greater than the basis amount. At this time, the final year of depreciation is adjusted so that the total of depreciation equals the basis amount.

The formula for flat‑rate depreciation is:

Depreciation Charge = Depreciable Basis * Flat‑Rate Percentage

Depreciable Basis = Cost – Salvage Value

When the sum of depreciation is greater than the basis amount, you use the following equation to calculate the last year of depreciation:

Depreciation Charge = Depreciable Basis – Accumulated Depreciation

Example: A company purchases a $20,000 car that has a $2,000 salvage value and a five-year service life. The annual flat‑rate is 23.6%.

Flat‑Rate Depreciation Schedule illustrates the flat‑rate depreciation schedule.

Flat‑Rate Depreciation Schedule

Year | Flat‑Rate | Calculation | Depreciation Expense | Accumulated Depreciation |

1 | 23.6% | $18,000 * 23.6% | $4,248 | $4,248 |

2 | 23.6% | $18,000 * 23.6% | $4,248 | $8,496 |

3 | 23.6% | $18,000 * 23.6% | $4,248 | $12,744 |

4 | 23.6% | $18,000 * 23.6% | $4,248 | $16,992 |

5 | | $18,000 ‑ $16,992 | $1,008 | $18,000 |

In year 5, the accumulated depreciation exceeds the asset depreciable basis. The depreciation charge is adjusted in year 5.

Units of Production

The units of production (UOP) method calculates depreciation based on items produced or units consumed from the asset. The formulas for units of production are:

Depreciation Per Unit of Production = Depreciable Basis / Total Units of Production

Depreciable Basis = Cost – Salvage Value

Depreciation Charge = Units of Production Per Period * Depreciation Per Unit of Production

Example: A company purchases a $25,000 stamping machine with a $2,000 salvage value. The machine is expected to produce 150,000 units over its service life. The depreciation per unit of production is:

$25,000 – $2,000 / 150,000 = $0.15 per unit

Units‑of-Production Depreciation Schedule illustrates the units‑of‑production depreciation schedule for 5 years.

Units‑of-Production Depreciation Schedule

Year | Units of Production Per Period | Calculation | Depreciation Expense |

1 | 30,000 | 30,000 * $0.15 | $4,500 |

2 | 25,000 | 25,000 * $0.15 | $3,750 |

3 | 20,000 | 20,000 * $0.15 | $3,000 |

4 | 40,000 | 40,000 * $0.15 | $6,000 |

5 | 30,000 | 30,000 * $0.15 | $4,500 |

Important: Beginning with QAD Enterprise Edition 2014, you can run the Fixed Assets module in Desktop mode. The only case where you must run the screen in Terminal mode is in Fixed Asset Maintenance (32.3) when an asset has a depreciation based on units of production.

Custom Table

You can substitute custom depreciation tables for the standard depreciation methods for calculating depreciation. Depreciation is calculated by specifying a depreciation factor for each period and year of the asset life. The depreciation factors are user‑defined and must equal 100% at the end of the asset service life.

The formulas for custom table are:

Depreciation Charge = Depreciable Basis * Depreciation Factor

Depreciable Basis = Cost – Salvage Value

Example: A company purchases a $10,000 computer that has a $2,000 salvage value and a four-year service life. The depreciation factors for each year of the asset service life are:

Custom‑Table Depreciation Factors

Year | Depreciation Rate |

1 | 7.0% |

2 | 9.5% |

3 | 27.0% |

4 | 56.5% |

Total | 100.0% |

Custom‑Table Depreciation Schedule illustrates the custom‑table depreciation schedule.

Custom‑Table Depreciation Schedule

Year | Depreciation Rate | Calculation | Depreciation Expense |

1 | 7.0% | $8,000 * 7.0% | $560 |

2 | 9.5% | $8,000 * 9.5% | $760 |

3 | 27.0% | $8,000 * 27.0% | $2,160 |

4 | 56.5% | $8,000 * 56.5% | $4,520 |