Tax Zone Hierarchies

A separate tax zone is required for each country, state, province, county, city, and postal zone that has distinct tax reporting requirements. Since one tax zone can include reporting and tax calculations for another, tax zones are organized into hierarchies. Set up higher-level zones before lower-level ones. For example, set up countries before their component states, states before counties, and so on.

How you set up a tax zone depends on its position in the hierarchy. To include a tax zone in the tax total and reporting for another zone, specify the first zone’s sums-into zone. The sums-into zone can be at a higher level or at the same level.

For example, a city tax zone included in provincial tax reporting sums into the provincial tax zone. Or, a tax zone for a suburb included in metropolitan tax reporting sums into the city tax zone. In the tax zone record, specify whether the first zone has its own subtotal on the main report and whether it also has its own reporting.

Tax Zone Hierarchies

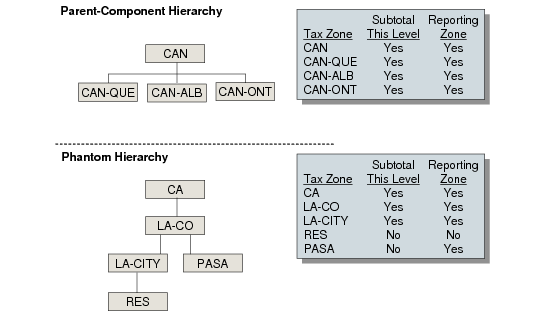

Tax Zone Hierarchies illustrates two hypothetical tax zone hierarchies.

• Parent-Component Hierarchy. The Canadian provinces Quebec, Alberta, and Ontario are subject to both federal and provincial taxes. The component tax zones CAN-QUE, CAN‑ALB, and CAN-ONT sum into zone CAN. All four zones are reporting zones in their own right and are subtotaled.

• Phantom Hierarchy. Reseda, a suburb of Los Angeles, is taxed in the same way as Los Angeles and does not have a subtotal on the city tax report. Tax zone RES sums into LA-CITY but is not subtotaled and is not a separate reporting zone.

Pasadena is subject to Los Angeles county tax and does not have a subtotal on the county tax report. Tax zone PASA sums into zone LA‑CO. It is not subtotaled but is a distinct reporting zone.